The U.S. housing market is under growing strain. Costs of ownership and renting are stretching household budgets to breaking points.

For real estate investors, this isn’t just a crisis—it’s a directional signal. Where affordability falters, opportunity emerges: rental demand shifts, novel home-ownership paths are needed, and supply shortfalls open ways to back durable, mission‐aligned assets.

This is about solving structural stresses, generating institutional quality income, and positioning for long-term returns in unmet markets.

The Affordability Baseline

To understand where value lies, first consider the current (2023-2025) data on cost burdens and supply constraints.

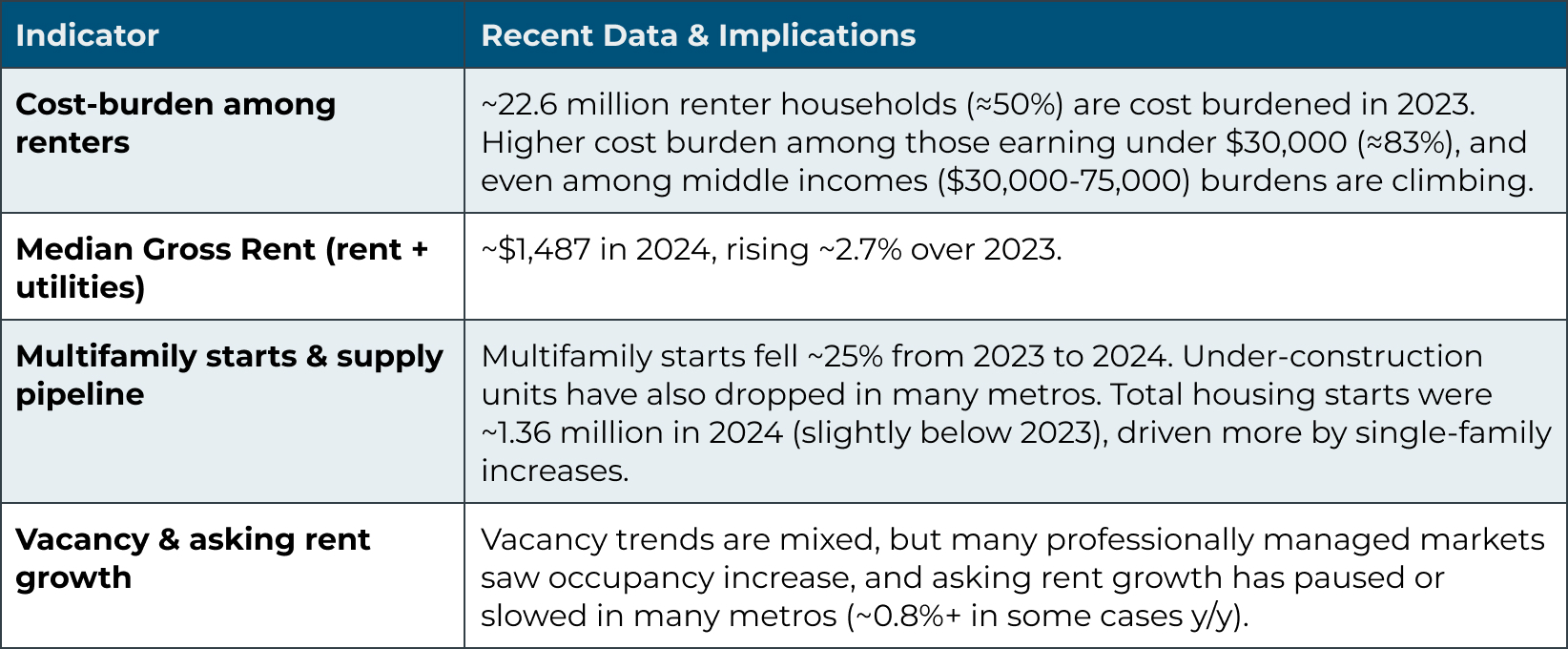

- Renters Under Pressure: As of 2023, about 50% of renter households—roughly 22.6 million of ~42.5 million renters—were cost-burdened, meaning they spent more than 30% of their income on rent and utilities. Among those, over 12 million are “severely cost burdened,” paying more than 50% of income towards shelter.

- Homeowners Are Also Strained: Rising home‐values, insurance, taxes, and high mortgage costs have pushed many homeowner households into cost burdens. While reliable figures for 2024 ownership cost burdens are less uniformly reported, the trend is clear: middle and lower income homeowners are increasingly stretched. (We’ll see the implications later in rent vs own tradeoffs.)

- Rents and Inflation Outpacing Household Incomes: The median gross rent (rent + utilities) rose to about US$1,487 in 2024, up ~2.7% from 2023 (inflation-adjusted). Meanwhile, for many renters incomes have not kept pace with rising shelter costs.

- Supply Weakness & Supply Mismatch:

- Multifamily starts are declining. For instance, total multifamily housing starts dropped about 25% year-over-year in 2024 from 2023.

- Permits and under-construction inventory are also down in many markets.

- Completion volume has hit record levels in some metros, but much of the new stock is high amenity / high rent, often priced out of reach for many households.

- Multifamily starts are declining. For instance, total multifamily housing starts dropped about 25% year-over-year in 2024 from 2023.

Why This Structural Stress Creates Investable Demand

These trends are not transient: they represent shifting demographic, financial, and regulatory dynamics. For institutional or large-scale capital, several demand pivots are especially material.

- Renter Growth Accelerates

As ownership becomes more expensive (mortgage rates, down payments, taxes, insurance), households either delay or forego ownership. More renters means more demand for professionally managed rental stock. - Cost Burden Moves Up the Income Ladder

The crisis is not only for low‐income renters. Middle-income households (e.g. incomes $30,000-$75,000) are increasingly cost burdened. That expands the addressable market for “attainable rentals” beyond just “low income / subsidized” segments. - Gap in Affordable New Supply

New supply is skewed toward high rents: luxury amenities, premium finishes, higher‐cost locations. Meanwhile, units with modest rents (e.g. under ~$1,500 depending on metro) are not keeping pace with demand. Supply constraints here create pricing power and lower downside risk for well-located, modest cost stock. - Regulatory and Policy Tailwinds

Housing affordability is increasingly a policy priority. Zoning reforms, tax incentives, subsidies, and mandates in many cities are pushing toward denser, mixed-use, and attainable housing. For investors, that means potential public/private partnership opportunities and regulatory supports that partially de-risk projects.

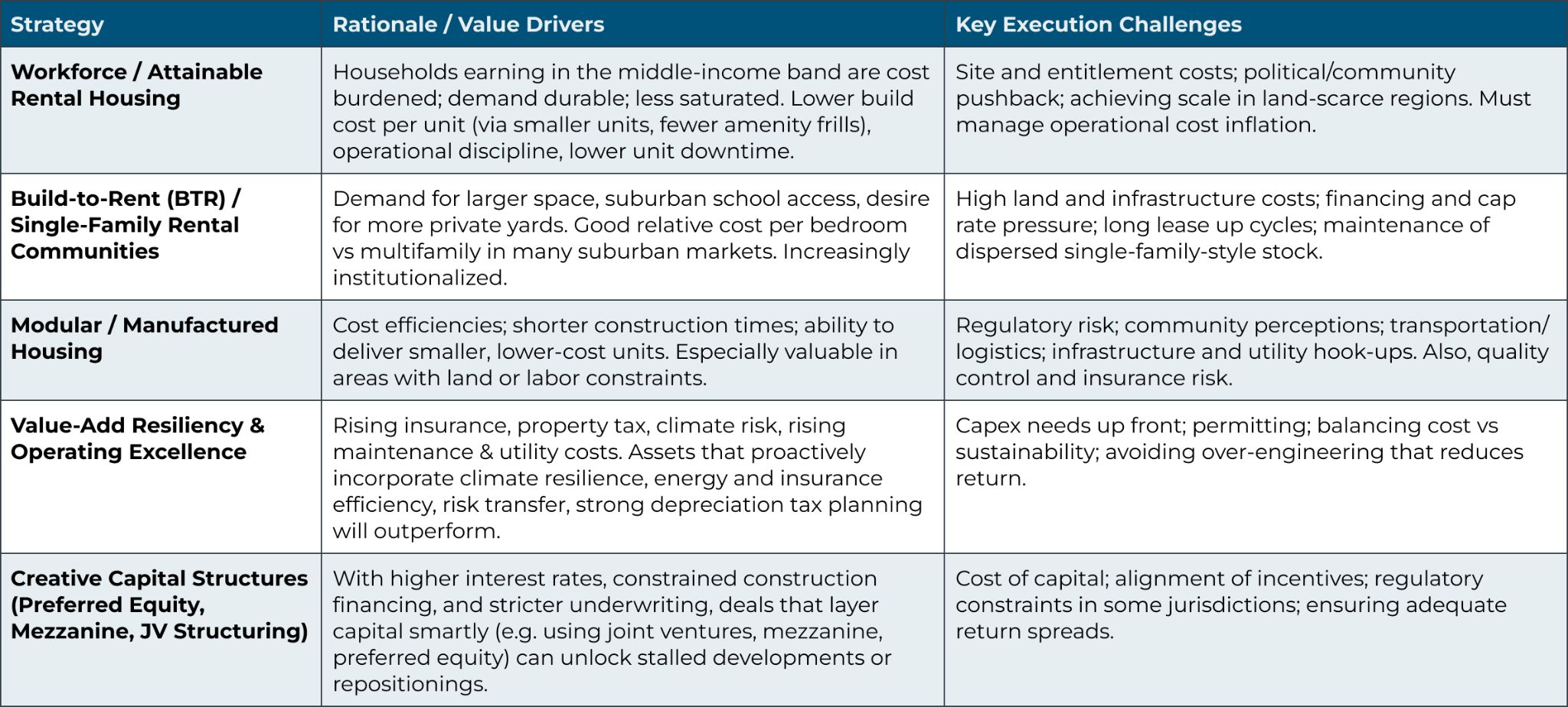

Where Investors Can (and Should) Lean In

To capture upside in this environment, certain product types and strategies look especially compelling. Here are high-conviction areas:

Updated Underwriting Implications & Risk Factors

In this environment, underwriting needs to adapt. Here’s what to focus on:

- Rent Growth & Vacancy: Rent growth has moderated in many markets. For example, professionally managed asking rents rose only ~0.8% y/y in Q1 2025 in many cases. Meanwhile vacancies are starting to drop in many metros—some with declining supply pipelines. These dynamics favor projects with short to medium term lease up horizons in markets where supply is thinning.

- Expense Inflation: Insurance, property taxes, labor, utilities and maintenance costs are rising faster than CPI. Budget stress for landlords is real. Assets in secondary/high-risk geographies (e.g. high natural hazard zones, wildfire, flood, hurricane risk) face outsized exposure. Hardening assets, better coverages, resilient design are differentiators.

- Capital Costs & Financing Constraints: Elevated interest rates, uncertain debt markets, and rising cost of debt or mezzanine equity mean that returns must be more conservatively modeled. That includes yield compression, longer holding periods, higher capital reserves.

- Regulatory / Policy Risk: Changes in zoning, inclusionary housing requirements, rent control (or rent stabilization), property tax changes, building and energy codes can materially affect returns. Local politics matter more than ever. Stack up scenario stress testing for potential regulatory headwinds.

- Geographic & Submarket Selection: Not all metros are equally exposed. Those with strong job growth, restrictions on supply, high in-migration, and favorable regulatory climate are better bets. Secondary/suburban markets may offer land, but must be evaluated carefully for infrastructure, amenity access, and services.

Updated Data & Key Market Indicators (2024–H1 2025)

To ground the above, here are updated data points and market signals that matter for decision making now:

Where the Value Is Greatest (for Principals, LPs, and Allocators)

Given the foregoing, the areas where institutional capital can expect the strongest risk-adjusted returns are:

- Tier 2 / 3 Cities & Suburban Edges — Lower land cost, fewer regulatory constraints, better affordability for renters. Submarkets with job growth and infrastructure investment are especially attractive.

- Attainable Rentals, Not Luxury — Units aimed at moderate income levels (~60-80% AMI, or equivalent in non‐government aligned rents) that deliver good amenities and strong unit economics.

- BTR / Single-Family Rental Platform Scale — Already seeing institutional flows; platforms that can aggregate scale, reduce per unit capex, manage dispersed maintenance and leverage technology will compete well.

- Alternative Construction Methods — Manufactured housing, modular, factory built — to reduce both cost and construction time. Could be critical in regions with labor shortages or high labor/land costs.

- Capital Stack Innovation & Risk Mitigation — Use of mezzanine debt, preferred equity, tax credits (LIHTC, opportunity zones, etc.), parametric insurance or risk transfer for climate and hazard risk, and ESG / decarbonization value adds where relevant.

- Focus on Operational Excellence & Resilience — Energy efficiency, solar/green design, water optimization, insurance cost management, preventative maintenance — these improve NOI stability, lower operating risks, and often appeal to both tenants and regulators/incentives.

Key Risks & Stress Tests

To be realistic, here are major risk vectors and what to stress in underwriting:

- Interest rate volatility (especially for construction debt); rising rates can depress demand for ownership, but also increase debt service for leveraged deals.

- Inflation in non-rent cost centers: insurance premiums, real property taxes, utilities, maintenance, labor.

- Regulatory change: rent control / stabilization, property tax increases, tougher energy/climate laws, permitting delays.

- Tenant affordability stress: if macro conditions worsen (job losses, wage stagnation, inflation), even middle income renters may pause relocation or face payment challenges.

- Construction cost surprises & supply chain disruptions.

- Location risk: infrastructure, access to jobs/transport, demographic tailwinds.

Conclusion

The affordability crisis is not merely a social issue—it is shaping capital flows. For real estate private equity, family offices, institutional LPs, and active or aspiring allocators, the opportunity lies where demand is highest, risk is manageable, and supply is constrained. Attainable housing (rental or hybrid ownership models), creative financing, resilient asset design, and operational discipline are the levers that separate winners from the pack.

If you want weekly, pragmatic insight on where cost pressures and capital are actually converging, subscribe to Carbon Weekly—CLICK HERE.

FAQs

Below are frequently asked questions from LPs, deal makers, and experienced sponsors navigating this environment.

Q1: What defines “attainable rental housing,” and is it profitable compared to luxury or higher-end multifamily?

Attainable rental housing generally refers to units aimed at middle‐income households (often earning 60-120% of Area Median Income, or incomes below the luxury bracket), with modest amenities, lower per-unit costs, and stable demand. While margins per unit or per square foot may be lower than luxury, risk is typically reduced: fewer vacancy swings, less demand elasticity, better resiliency in downturns. In many metros, rent growth in non-luxury tiers has been more stable. Proper cost control and scale matter heavily.

Q2: Are there particular regions or metros that offer better opportunity given regulatory and supply trends?

Yes. Regions with strong job growth, favorable land cost, and more permissive zoning tend to outperform. Also, many Tier 2 or 3 cities and suburban edges (especially in the Southeast, Southwest, and parts of the Midwest) are seeing in-migration and infrastructure investment, but are less saturated. Evaluate local property tax policies, insurance risk, and zoning/regulation environment when choosing locations.

Q3: How much does the rising cost of insurance and climate risk factor into underwriting now?

It’s substantial and growing. Insurance premiums in many markets have increased significantly over recent years. Assets in catastrophe zones (wildfire, flood, hurricane, etc.) are seeing insurance costs, deductibles, and required resiliency measures rise. Underwriting dialogues now typically include quantification of climate risk exposure, cost of mitigation, and effects on asset valuations and NOI. Parametric insurance, risk transfer tools, and resilient design/retrofit are increasingly part of the competitive edge.

Q4: What return expectations are realistic in this market, given all the inflation, capital cost, and regulatory headwinds?

Return expectations vary by strategy and risk. For fully stabilized attainable rental assets in favorable markets, net IRRs might be lower than luxury or high-risk development plays, but risk-adjusted returns (including income yield, stability, and exit potential) remain strong. For value‐add or development / build-to-rent, required return spreads need to account for cap rate compression, construction risk, and soft cost inflation. LPs and sponsors should model downside (longer lease up, higher vacancy, higher expenses) and preserve margin via conservative leverage.

Q5: Are there tax or policy incentives that materially help in these kinds of deals?

Yes. Some of the key levers: Low-Income Housing Tax Credits (LIHTC), Opportunity Zones, state/local incentives for affordable housing, inclusionary zoning incentives, tax abatement for certain use types, historic or other rehab credits, and sometimes renewable energy or efficiency credits. Lastly, policy at municipal and state levels to ease permitting, increase allowable density, or reduce impact/property tax burden can be just as powerful financially.

Q6: How can family offices or smaller LPs compete in what’s becoming an institutional domain (BTR platforms, modular, etc.)?

Smaller LPs or family offices can succeed by:

- Niche specialization: Focus on a submarket or product type (e.g. manufactured housing, modular, attainable rentals) where competition is less intense.

- Partnerships & JVs: Align with platform managers, bring capital + deal sourcing + local knowledge.

- Operational excellence: Strong cost discipline, lean management, technology adoption.

.svg)